![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

48 Cards in this Set

- Front

- Back

|

Return On Investment |

|

|

|

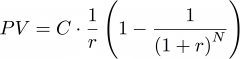

Present Value of Annuity for n Periods |

|

|

|

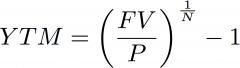

Yield to Maturity of an n-Year Zero-Coupon Bond |

|

|

|

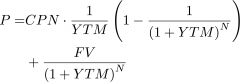

Yield to Maturity of an n-Year Coupon Bond |

|

|

|

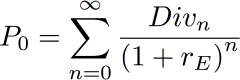

Dividend-Discount Model: Current Stock Price |

|

|

|

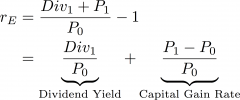

Dividend-Discount Model: Total Return |

|

|

|

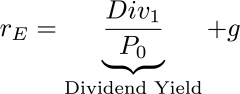

Dividend-Discount Model: Total Return with constant growth |

|

|

|

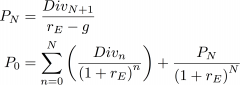

Dividend-Discount Model: with Constant Long-Term Growth |

|

|

|

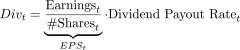

Dividend, given EPS and Divident-Payout Rate |

|

|

|

Growth, given Retention Rate and ROI |

OBS: Rentation at t => growth for year t+1 |

|

|

Stock Price in Total Payout Model |

|

|

|

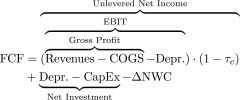

Unlevered Free Cash Flow |

|

|

|

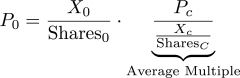

Price, in Free Cash Flow Valuation Model |

|

|

|

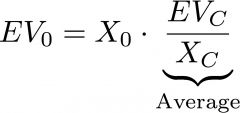

Enterprise Value |

|

|

|

Price based on Multiple |

|

|

|

Valuation Based on Multiples (EV) |

|

|

|

NWC |

|

|

|

After-Tax Cash Flow from Asset Sale |

|

|

|

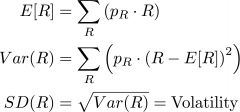

Expected Returns, Variance, and Volatility |

|

|

|

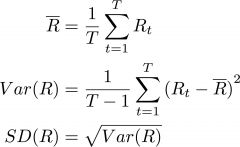

Average Return, Variance, and Volatility based on Historical Returns |

|

|

|

Realized Annual Returns assuming Reinvestment |

|

|

|

Types of Risk |

* The total risk of a security represents both idiosyncratic (or independent, firm-specific, unique, diversifiable) risk * systematic (or common, market, undiversifiable) risk. |

|

|

Stock beta |

|

|

|

CAPM |

|

|

|

Covariance based on Historical Data |

|

|

|

Correlation |

|

|

|

Expected Return of Debt |

|

|

|

CAPM for Bonds |

|

|

|

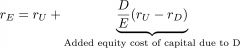

Unlevered Cost of Capital (Pretax-WACC) |

|

|

|

Debt-Equity-Ratio |

|

|

|

MM Proposition I |

In a perfect capital market, the total value of a firm is equal to the market value of the total cash flows generated by its assets and is not affected by its choice of capital structure. |

|

|

MM Proposition II |

The cost of capital of levered equity increases with the firm's market value debt-equity ratio |

|

|

Trade-Off Theory |

|

|

|

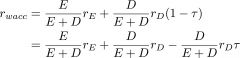

(effective after-tax) WACC |

|

|

|

WACC Method |

1. Determine the free cash flow of the investment. 2. Compute the weighted average cost of capital. 3. Compute the value of the investment,including the tax benefit of leverage, by discounting the free cash flow of the investment using the WACC. |

|

|

Debt capacity |

|

|

|

APV Method |

1. Determine the investment's value without leverage, V_U, by discounting it' s free cash flows at the unlevered cost of capital, r_U. 2. Determine the present value of the interest tax shield. 2a. Determine the expected interest tax shield: Given expected debt capacity D_t on date t, the interest tax shield on date t + 1 is \tau_c \cdot r_D \cdot D_t. 2b. Discount the interest tax shield using r_U. 3. Plug into the APV Formula. |

|

|

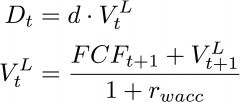

Interest tax shield given Debt Capacity |

|

|

|

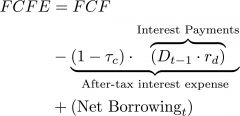

FCFE |

|

|

|

Net Borrowing |

|

|

|

FCFE Method |

1. Determine the FCFE 2. Discount at the project's equity cost of capital. |

|

|

Post-money Valuation |

Post-money Valuation = Pre-Money Valuation + Amount Invested |

|

|

IPO Puzzels

|

1. IPOs are underpriced on average. 2. New issues are highly cyclical. 3. The transaction costs of an IPO are high. 4. Long-run performance after an IPO is poor on average. |

|

|

Debt-to-Value Ratio |

d = \frac{D}{D+E} |

|

|

Growth vs. Value Stock |

Analysts oftenclassify firms with low market-to-book ratios as value stocks (shares), and those with highmarket-to-book ratios as growth stocks (shares). |

|

|

Bonds trading at premium, discount and at par. |

Discount: FV > P Par: FV = P Premium = FV < P |

|

|

Opportunity Costs |

Costs on resource that the firm already owns. The resource could provide value for the firm in another opportunity or project. |

|

|

Project externalities |

Indirect effects of the project that may increase or decrease the profit of other business activities. E.g.: cannibalisation. |