![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

75 Cards in this Set

- Front

- Back

|

Externality |

Cost or benefit from either production or consumption that falls on someone other than the producer or consumer |

|

|

Negative externality |

imposes external cost |

|

|

Positive externality |

provides an external benefit |

|

|

Examples of Negative Production Externalities |

Logging, Airplane Noise, and Pollution |

|

|

Examples of Negative Consumption Externalities |

Smoking, and Loud Parties |

|

|

Examples of Positive Externalities |

Flu vaccination |

|

|

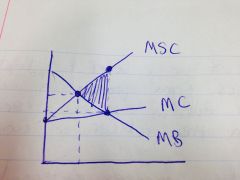

Marginal Social Cost |

Marginal Cost incurred by the entire society |

|

|

MSC Formula |

MSC=Marginal Cost + Marginal external cost |

|

|

Marginal Cost is borne by |

the producer |

|

|

External Cost is borne by |

other than the producer |

|

|

When is it efficient? |

MSC=MB Marginal Social Cost = Marginal Benefit |

|

|

Coase Theorem |

If property rights exist and only small # of people and low transaction costs, then it is efficient. |

|

|

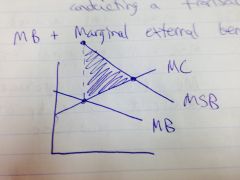

MSB formula |

MSB = MB + Marginal external benefit |

|

|

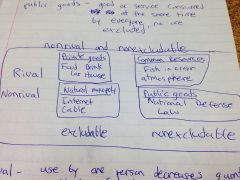

Rival |

Use by one person decreases # available for others |

|

|

Excludable |

Possible to prevent someone from enjoying the benefits |

|

|

Public Goods |

Non-Rival, and Non-Excludable |

|

|

Common Resources |

Rival, and Non-Excludable |

|

|

Natural Monopoly |

Non-Rival, and Excludable |

|

|

Private Goods |

Rival and Excludable |

|

|

Memorize the Chart for private good etc.

|

|

|

|

Graph for MSC

|

|

|

|

Graph for MSB

|

|

|

|

Examples of Private Goods |

Food, Drink, Car, House |

|

|

Examples of Common Resources |

Fish in the ocean, the atmosphere |

|

|

Examples of Natural Monopoly |

Internet, and Cable |

|

|

Examples of Public Goods |

National Defense, and The Law |

|

|

Demand curve for public goods |

Summed vertically |

|

|

Demand curve for private goods |

Summed Horizontally |

|

|

Tragedy of Commons |

Overuse of a common resource when its users don't conserve |

|

|

Short Run |

time-frame in which quantities of some resources are fixed. |

|

|

Marginal Product formula |

MP= ^TP/^QL Change in Total Product divided by Change in Quantity of Labor |

|

|

Total Product |

Total quantity of a good produced in a given period |

|

|

Increasing Marginal Returns |

Additional worker exceeds the marginal product of the previous worker |

|

|

Decreasing Marginal Returns |

Additional workers marginal product is less than the previous worker |

|

|

Graph of Average costs

What equals what? |

Space between AVC and ATC are the same as AFC. |

|

|

Long run |

All costs are variable |

|

|

Economies of Scale |

Average Total Cost falls as output increases |

|

|

Diseconomies of Scale |

Average Total Cost rises as output increases |

|

|

Constant Returns to Scale |

Average Total Cost is constant |

|

|

Long Run Average Cost Curve

(LRAC) |

Take the lowest portions of all ATC curves

|

|

|

Price Taker |

Can't influence the price

|

|

|

4 Characteristics of Perfect Competition |

1. No Barriers to entry 2. No Advantage 3. Identical Products 4. Well informed buyers and suppliers |

|

|

Monopoly |

No close substitute Barrier to Entry |

|

|

Monopolistic Competition |

Slightly different products |

|

|

Oligopoly |

Almost identical products Small number of firms

|

|

|

Marginal Revenue in Perfect Competition |

MR=Price |

|

|

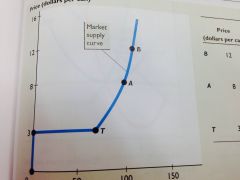

Shutdown Point |

Both at minimum AVC |

|

|

Supply Curve of Shutdown point

|

Upload Photo.

|

|

|

Entry to Long Term |

Entry increases supply and lowers the price and increase in demand raises price.

Supply and Demand Curves shift to the Right. |

|

|

Exit from Long Term |

Exit decreases supply and raises price and decrease in demand lowers price.

Supply and Demand Curves shift to the Left. |

|

|

Monopoly Barriers |

Natural Monopoly Ownership Legal

|

|

|

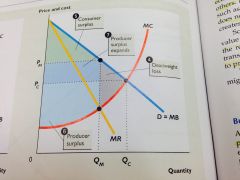

Demand and Marginal Revenue Curve in a Monopoly

|

|

|

|

Monopoly produces a deadweight loss

|

|

|

|

When demand is elastic Marginal Revenue is |

Positive |

|

|

When demand is inelastic Marginal Revenue is |

Negative |

|

|

Difference between private cost and social cost? |

Private cost only considers cost borne by producers |

|

|

Property rights force |

Marginal Private Cost to = Marginal Social Cost |

|

|

If a firm pollutes a river the government can... |

Impose a pollution tax that equals the Marginal external cost |

|

|

If marginal external cost is $10 per ton, and firm is unregulated then... |

Marginal Social Cost will be $10 more than Marginal Benefit |

|

|

Possible solutions to Tragedy of Commons |

Setting Production Quota Granting Individual Transferable Quotes Establishing Property Rights to the Resource

|

|

|

The U-Shape reflects |

Increasing and Decreasing Marginal Returns |

|

|

How to find Fixed Cost |

The Cost at 0 workers |

|

|

How to find Variable Cost |

Total Cost - Fixed Cost |

|

|

To maximize profits make |

Price = Marginal Cost |

|

|

A perfectly competitive firm will survive if it has |

price at least equal to AVC |

|

|

Short Run to increase profit must |

Increase Labor Quantity |

|

|

If producing a good creates pollution in an unregulated market then marginal social cost is |

greater than equilibrium price |

|

|

Diseconomies of scale can occur from |

Management difficulties as the firm increases its size |

|

|

A perfectly competitive firm can sell all of |

its output at market price |

|

|

Elasticity of Perfectly competitive firms |

Perfectly Elastic because they are price-takers |

|

|

If a firm shuts down the price is |

less than minimum AVC |

|

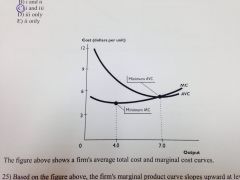

Based on figure, the firms marginal product curve slopes upward at levels of output between _________ and the firms average product curve slopes upward at levels of output between ________ |

0 and 4.0, 0 and 7.0

|

|

|

When marginal revenue is positive, total revenue __________ when output increases and demand is __________ |

Increases; Elastic |

|

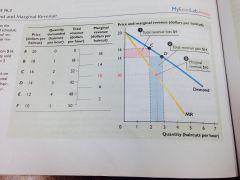

Christy's Haircuts, faces the demand schedule shown above. What is marginal revenue of the 25th haircut |

$5.00

|

|

|

To maximize its profit, a perfectly competitive firm produces so that _______ and a single-price monopoly produces so that _________. |

MR = MC; MR = MC |