![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

92 Cards in this Set

- Front

- Back

- 3rd side (hint)

|

Business Finance |

Study how you manage your money |

|

|

|

Business |

Putting up |

|

|

|

Finance |

Capital |

|

|

|

Shared Capital Loan Capital |

Sources of Capital for corporation |

|

|

|

Business |

Venturing |

|

|

|

Finance |

Money and its management Allocation of resources |

|

|

|

Financial institutions Investments Business Finance |

Three areas of finance |

|

|

|

Financial institutions |

Creation |

Area of finance |

|

|

Investment |

Analysis and planning |

Area of finance |

|

|

Business Finance |

Management |

|

|

|

1. Allocation of funds 2. Procurement of funds 3. Utilization of funds |

Functions of Business Finance |

|

|

|

Allocation of funds |

Profitable Minimal cost |

Function of BF |

|

|

Procurement of funds |

Evaluation of funds Short term/ long term |

Function of BF |

|

|

Efficient - periodic assessment Effective - short/long term goals |

Utilization of funds |

|

|

|

Efficient |

Periodic assessment |

|

|

|

Effective |

Short/long term goals |

|

|

|

1. To acquire necessary funds to ensure that they are used effectively. 2. Capital budgeting 3. Capital structuring 4. Working capital management |

Roles of financial manager |

|

|

|

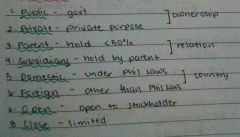

Sole proprietorship Partnership Corporation |

Business Organization |

|

|

|

Sole proprietorship |

One owner; DTI; BIR |

|

|

|

Department of Trade and Industry |

DTI |

|

|

|

Bureau of Internal Revenue |

BIR |

|

|

|

Partnership |

Owned by two or more; SEC |

|

|

|

Securities and Exchange Commission |

SEC |

|

|

|

Corporation |

Stock; SEC Dividends |

|

|

|

General Limited |

Types of partnership |

|

|

|

General |

All liabilities |

|

|

|

Limited |

No liability No active role |

|

|

|

Universal Particular General Limited Capital Industrial Capitalist industrial |

Classification of partnership |

|

|

|

Universal |

All (object of contribution) |

|

|

|

Particular |

Determined (object of contribution) |

|

|

|

Capital |

Money |

Classification of partnership |

|

|

Industrial |

Work/services |

Classification of partnership |

|

|

Capitalist Industrial |

Both money and work |

Classification of partnership |

|

|

Stock - profit Non-stock - non profit |

Classification of corporation according to sources of capital |

|

|

|

Classification of Corporation |

|

|

|

1. Voting Right 2. Ownership 3. Transfer of ownership 4. Entitlement of dividend 5. Right to sue 6. Pre-emptive right |

Rights of stockholder |

|

|

|

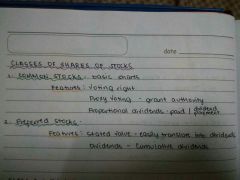

Classes of shares of stocks |

|

|

|

Class a |

Filipino stocks |

|

|

|

Class b |

Foreign stocks |

|

|

|

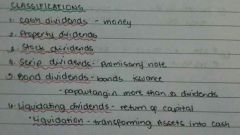

Dividends |

Value received by the stockholders |

|

|

|

Classifications of dividends |

|

|

|

Liquidation |

Transforming assets into cash |

|

|

|

1. Declaration 2. Ex-dividend date 3. Date of Record 4. Payment date |

Dividend payment (step) |

|

|

|

1. Equity Capital Stock 2. Borrowed Capital 3. Debt Financing/ Borrowings |

Sources of Capital |

|

|

|

Equity |

*Source of capital for sole proprietorship *venture capitalist |

|

|

|

Venture Capitalist |

Firm na nagpapautang in exchange of equity |

|

|

|

Capital Stock |

*Source of capital fo corporation *Stock market |

|

|

|

Borrowed Capital |

Loans, there is interest |

|

|

|

1. Not required to cash dividends 2. It has a maturity date |

Advantage of Equity= stocks |

|

|

|

Control and ownership are being affected |

Disadvantage of equity= stocks |

|

|

|

Authorized Capital Issued Stock Reacquired Stock Outstanding Stock |

Forms of Capital Stock |

|

|

|

Authorized Capital |

Maximum number of shares |

Form of capital stock |

|

|

Issued stock |

Subscribed authorized stock |

Form of capital stock |

|

|

Reacquired Stock |

By gift Buying back - forfeiture of stock |

Form of capital stock |

|

|

Outstanding stock |

Portion of issued stock |

Form of capital stock |

|

|

Common stock Preferred stock |

Classes of Stock |

|

|

|

Common stock |

Basic shares |

|

|

|

Preferred stock |

Stocks with preference |

|

|

|

Debt financing |

Borrowings |

|

|

|

Keme of Debt Financing |

|

|

|

1. Trade credit market - raw materials; manufacturer/ distributor 2. Customer loan market - banks; creditors; finance company |

Major Sources of funds |

|

|

|

Equity vs Debt Capital |

|

|

|

Loans |

Lending of money |

|

|

|

Amortization |

Allocation of cost |

|

|

|

1. Pure-discount loan - simplest form 2. Interest-only loan - interest paid 3. Amortized loan - repaid in parts |

Kinds of loans |

|

|

|

Working capital |

To finance its day to day transactions |

|

|

|

Working capital |

Portion of the firms capital continuously converted into cash |

|

|

|

Working capital |

Portion of the firms capital continuously converted into cash |

|

|

|

Firm's cash Checks for the encashment Bank account balances Accounts receivable Inventories Prepaid expense |

Woking capital includes |

|

|

|

1. Inventory replenishment 2. Provision for Operating Expenses 3. Back-up credit sales 4. Safety margin |

Why we need working capital? |

|

|

|

Inventory replenishment |

Sufficient stock of inventory |

|

|

|

Provision for operating expenses |

Back-up expenses |

|

|

|

Back-up credit sales |

Until receivables are converted inti cash |

|

|

|

Safety margin |

Unexpected expense Delays in cash inflows Decline in revenue |

|

|

|

-purchase and cash sales -time period from collection -time period from purchase or payment -accounts receivable collection -inventory investment |

The amount of cash needed may depend on: |

|

|

|

Cash-management |

Sufficient amount of profit must be attained |

|

|

|

Liquidity management |

Sufficient cash to cover cash requirements |

|

|

|

Inventory management |

Inventory turn over Earn profit/sales |

|

|

|

Accounts receivable |

Credit sales Money owed to the business |

|

|

|

Trade credit |

Credit sale made to other business Open account- no formal debt contract |

|

|

|

Consumer credit |

Credit sale made to other individual |

|

|

|

1. Credit period 2. Discount period 3. Discount rate |

Credit forms |

|

|

|

Credit period |

The date the buyer is invoiced/ date of payment |

|

|

|

Discount period |

Discount for prompt payment |

|

|

|

Discount rate |

Price reduction |

|

|

|

Short-term operations Long-term operations |

Financing decision |

|

|

|

Capital budgeting |

To plan and control |

|

|

|

Expenditures Valuation Investments |

Under capital budgeting |

|

|

|

Break-even point |

Variable and fixed expenses |

|

|

|

BEP= Sales income - expenses |

Formula for break-even point |

|

|

|

Variable expense |

Directly proportional Changing Labor cost |

|

|

|

Fixed expense |

Remain constant Not changing |

|