![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

36 Cards in this Set

- Front

- Back

|

La Crosse Partners LLC has a franchise agreement with Arnolds Crispy Fry that expires in seven years, but is renewable at each expiration date for a nominal fee. If the franchise agreement is initially valued at $60,000: A)amortization expense in the sixth year will be zero. B)an accelerated amortization method is more appropriate than the straight-line method. C)amortization expense in the first year will be one-seventh of $60,000. |

A Because the franchise agreement is renewable for a nominal fee, it is treated as an intangible asset with an indefinite life and therefore not amortized but tested for impairment regularly. |

|

|

A firm needs to adjust its financial statements for a change in the tax rate. Taxable income is $80,000 and pretax income is $120,000. The current tax rate is 50%, and the new tax rate is 40%. The effect on taxes payable of adjusting the tax rate is closest to: A)$8,000. B)$4,000. C)$16,000. |

A "Pretax income" denotes earnings before taxes for financial reporting. "Taxable income" is earnings before taxes for computing taxes payable, where taxes payable refers to the actual tax liability to the government. Since taxable income is $80,000, the difference in taxes payable is ($80,000)(0.5) - ($80,000)(0.4) = $8,000. |

|

|

Slovac Company purchased a machine that has an estimated useful life of eight years for $7,500. Its salvage value is estimated at $500.What is the depreciation expense for the second year, assuming Slovac uses the double-declining balance method of depreciation? A)$1,438. B)$1,406. C)$1,875. |

B double-declining balance depreciation rate = 2 × 1/8 = ¼ or 25%first year deprecation will be $7,500 × 0.25 = $1,875second year deprecation will be ($7,500 − $1,875) × 0.25 = $1,406 |

|

|

Deferred tax liabilities may result from: A)pretax income less than taxable income due to temporary differences. B)pretax income greater than taxable income due to permanent differences. C)pretax income greater than taxable income due to temporary differences. |

C Deferred tax liabilities result from temporary differences that cause pretax income and income tax expense (on the income statement) to be greater than taxable income and taxes due (on the firm's tax form). Temporary differences that cause pretax income to be less than taxable income are recognized as deferred tax assets. Permanent differences do not result in deferred tax items; instead they cause the effective tax rate to differ from the statutory tax rate. |

|

|

Which of the following situations will most likely require a company to record a valuation allowance on its balance sheet? A)To report depreciation, a firm uses the double-declining balance method for tax purposes and the straight-line method for financial reporting purposes. B)A firm is unlikely to have future taxable income that would enable it to take advantage of deferred tax assets. C)A firm has differences between taxable and pretax income that are never expected to reverse. |

B A valuation allowance is a contra account (offset) against deferred tax assets that reflects the likelihood that the deferred tax assets will never be realized. If a firm is unlikely to have future taxable income, it would be unlikely to ever use its deferred tax assets, and therefore must record a valuation allowance. |

|

|

Alter Inc. determines that it has $35,000 of accounts receivable outstanding at the end of 20X8. Based on past experience, it recognizes an allowance for bad debt equal to 10% of its credit sales. The tax base of Alter's accounts receivable at the end of 20X8 is closest to: A)$35,000.B)$31,500.C)$3,500. |

A For tax purposes, bad debt expense cannot be deducted until the receivables are deemed worthless. Therefore, the tax base is $35,000 since no bad debt expense has been deducted on the tax return. Note that the carrying value would be $31,500 since bad debt expense is reflected on the income statement. |

|

|

As part of a major restructuring of business units, General Security (an industrial conglomerate operating solely in the U.S. and subject to U.S. GAAP) recognizes significant impairment losses. The Investor Relations group is preparing an informational packet for shareholders, employees, and the media. Which of the following statements is least accurate? A)The write-downs are reported as a component of income from continuing operations. B)During the year of the write-downs, retained earnings and deferred taxes will decrease. C)Write-downs taken on asset values can be reversed in later years if market conditions improve. |

C ExplanationReferencesImpairments cannot be restored under U.S. GAAP. Both remaining statements are correct. |

|

|

A dance club purchases new sound equipment for $25,352. It will work for 5 years and has no salvage value. For financial reporting, the straight-line depreciation method is used, but for tax purposes depreciation is 35% of original cost in years 1 and 2 and the remaining 30% in Year 3. Annual revenues are constant at $14,384 over these five years. If the tax rate for years 4 and 5 changes from 41% to 31%, what is the deferred tax liability as of the end of year 3? A)$2,948.B)$1,039.C)$3,144. |

C Straight-line depreciation = $25,352 / 5 = $5,070. Income (years 1, 2, and 3) using straight-line depreciation = $14,384 − $5,070 = $9,314.Accelerated depreciation (years 1 and 2) = 0.35($25,352) = $8,873. Income (years 1 and 2) = $14,384 − $8,873 = $5,511.Accelerated depreciation (year 3) = 0.3($25,352) = $7,606. Income (year 3) = $14,384 − $7,606 = $6,778.Cumulative difference in income at end of year 3 = 3($9.314) − [2($5,511) + $6,778] = $10,142.DTL value at new tax rate = 0.31($10,142) = $3,144. |

|

|

Which of the following statements about deferred taxes is least accurate? Deferred taxes: A)may never "reverse" in the case of companies that are growing. B)can relate to either permanent or temporary differences. C)arise primarily due to differences between GAAP and IRS code. |

B Permanent difference will not result in deferred taxes since they are not expected to reverse in the future. |

|

|

On January 1, 2004, Cayman Corporation bought manufacturing equipment for $30 million. On December 31, 2006, Cayman determined the equipment was impaired and recognized a $5 million impairment loss in its income statement. As of December 31, 2007, the fair value of the equipment exceeded the book value by $7 million. What amount of the recovery in value can Cayman recognize in its 2007 income statement under U.S. Generally Accepted Accounting Principles (U.S. GAAP) and under International Financial Reporting Standards (IFRS)? U.S. GAAP;IFRS A)$0;$7 million B)$5 million;$7 million C)$0;$5 million |

C

U.S. GAAP does not permit upward valuations of plant and equipment. Under IFRS, the recovery is reported in the income statement to the extent that the previous downward adjustment (loss) was reported in net income. Otherwise, the increase in value is reported as an adjustment to equity. Thus, under IFRS, $5 million will be reported in 2007 net income and $2 million will be directly added to to equity (as an adjustment to equity). |

|

|

Which of the following statements regarding the capitalization of an expense is least accurate? A)Capitalizing an expense lowers current period net income. B)Capitalizing an expense creates an asset. C)Capitalized expenses increases equity.E] |

A

Capitalizing expenses reduces current period expenses by the amount capitalized. The amount capitalized is added to assets which increases equity by increasing net income and retained earnings in the current period. |

|

|

Which of the following statements regarding capitalizing versus expensing costs is least accurate? A)Total cash flow is higher with capitalization than expensing. B)Cash flow from investing is higher with expensing than with capitalization. C)Capitalization results in higher profitability initially. |

A Total cash flow is higher with capitalization than expensing is least accurate because total cash flow would be the same under both methods, not considering tax implications. |

|

|

Habel Inc. owns equipment with a tax base of $400,000 and a carrying value of $600,000. Habel also has a tax loss carryforward of $200,000 that is expected to be utilized in the foreseeable future. Deferred tax items on the balance sheet are valued based on a tax rate of 30%. If the tax rate increases to 35%, the adjustments to the value of deferred tax items will most likely cause Habel's total liabilities-to-equity ratio to: A)increase. B)remain unchanged. C)decrease. |

A The $200,000 difference between the tax base and the carrying value of the equipment gives rise to a taxable temporary difference that leads to a deferred tax liability of $60,000 ($200,000 × 30%). The tax loss carryforward of $200,000 leads to a deferred tax asset of $60,000 ($200,000 × 30%).The increase in the tax rate from 30% to 35% will increase both the DTL and the DTA by $10,000 ($200,000 × 5%). Equity is unchanged. Therefore, the total liabilities-to-equity ratio will increase because of the increase in the deferred tax liability. |

|

|

The revaluation model for investment property is permitted under:A)both IFRS and U.S. GAAP.B)neither IFRS nor U.S. GAAP.C)IFRS, but not U.S. GAAP. |

B For long-lived assets classified as investment property, IFRS allows either the cost model or the fair value model. The revaluation model is permitted for long-lived assets that are not classified as investment property. U.S. GAAP only permits the cost model for valuation of long-lived assets and does not identify investment property as a specific subset of long-lived assets. |

|

|

A company purchases a new pizza oven for $12,675. It will work for 5 years and have no salvage value. The company will depreciate the oven over 5 years using the straight-line method for financial reporting, and over 3 years for tax reporting. If the tax rate for years 4 and 5 changes from 41% to 31%, the deferred tax liability as of the end of year 3 is closest to:A)$1,040B)$1,570C)$2,080 |

B At the end of year 3, the oven has a tax base of zero (it has been fully depreciated for tax reporting) and a carrying value on the balance sheet of $12,675 - 3(0.2)($12,675) = $5,070. The deferred tax liability, valued at the 31% tax rate that will apply when the temporary difference reverses, is ($5,070 - $0)(0.31) = $1,571.70. |

|

|

If a firm overestimates its warranty expenses, which of the following results is least likely? A)Income tax expense will be greater than taxes payable. B)A deferred tax asset will result. C)A timing difference will result between tax and financial reporting. |

A Income tax expense will be less than taxes payable because the firm can only recognize warranty expense as they occur. Thus, if the warranty expenses are overestimated on the financial statements income tax expense will be less that taxes payable. |

|

|

U.S. GAAP least likely requires property, plant, and equipment to be tested for impairment:A)when events indicate the firm may not recover the asset's carrying value.B)when an asset is reclassified as held-for-sale.C)at least annually. |

C Under U.S. GAAP, a PP&E asset is tested for impairment when events and circumstances indicate the firm may not recover its carrying value through future use, or if the asset is reclassified from held-for-use to held-for-sale. Under IFRS, firms are also required to assess at least annually whether events and circumstances indicate impairment may have occurred. |

|

|

Selected information from Kentucky Corp.'s financial statements for the year ended December 31 was as follows (in $ millions):Property, Plant & Equip.10 Deferred Tax Liability0.6Accumulated Depreciation(4) The balances were all associated with a single asset. The asset was permanently impaired and has a present value of future cash flows of $4 million. After Kentucky writes down the asset, Kentucky's tax accounts will be affected as follows (the tax rate is 40%):A)deferred tax liability will be eliminated and deferred tax assets will increase $200,000.B)deferred tax liability will be eliminated and deferred tax assets will increase $1.4 million.C)taxes payable will decrease $800,000. |

A A permanently impaired asset must be written down to the present value of its future cash flows. The asset's carrying value of ($10 − $4 =) $6 million must be reduced by $2 million to $4 million. An impaired value write-down reduces net income for accounting purposes, but not for tax purposes until the asset is sold or disposed of, so taxes payable do not decrease. At a 40% tax rate, the eventual writedown for tax purposes of $2 million will cause $800,000 of changes in deferred tax items. The $600,000 deferred tax liability associated with this asset is eliminated and a deferred tax asset of $200,000 is established. |

|

|

An analyst gathered the following information about a company:Taxable income = $100,000.Pretax income = $120,000.Current tax rate = 20%.Tax rate when the reversal occurs will be 10%.What is the company's tax expense?A)$10,000.B)$22,000.C)$24,000. |

B Deferred tax liability = (120,000 − 100,000) × 0.1 = 2,000Tax expense = current tax rate × taxable income + deferred tax liability0.2 × 100,000 + 2,000 = 22,000 |

|

|

A health care company purchased a new MRI machine on 1/1/X3. At year-end the company recorded straight-line depreciation expense of $75,000 for book purposes and accelerated depreciation expense of $94,000 for tax purposes. Management estimates warranty expense related to corrective eye surgeries performed in 20X3 to be $250,000. Actual warranty expenses of $100,000 were incurred in 20X3 related to surgeries performed in 20X2. The company's tax rate for the current year was 35%, but a tax rate of 37% has been enacted into law and will apply in future periods. Assuming these are the only relevant entries for deferred taxes, the company's recorded changes in deferred tax assets and liabilities on 12/31/X3 are closest to:DTA;DTL A)$55,500;$6,650 B)$52,500;$6,650 C)$55,500;$7,030 |

C DTL = (tax depreciation - financial statement depreciation) × future tax rate= ($94,000 - $75,000) × 37% = $7,030.DTA = (estimated warranty expense − actual warranty expense) × future tax rate = ($250,000 − $100,000) × 37% = $55,500. |

|

|

For impaired long-lived assets, a firm reporting under IFRS is least likely required to disclose the: A)amounts of impairment losses and reversals by asset class. B)circumstances that caused the impairment losses or reversals. C)estimated probabilities of reversing impairment losses. |

C ExplanationReferencesUnder IFRS, firms with impaired assets must disclose the amounts of impairment losses and reversals by asset class, the circumstances that caused the impairment losses or reversals, and where the losses or reversals are recognized on the income statement. |

|

|

A company acquires an intangible asset for $100,000 and expects it to have a value of $20,000 at the end of its 5-year useful life. If the company amortizes the asset using the double-declining balance method, amortization expense in year 4 of the asset's useful life is closest to: A)$6,910.B)$1,600.C)$8,640. |

B Net book value at the end of year 3 is $100,000 × 3/5 × 3/5 × 3/5 = $21,600. DDB amortization in year 4 of 2/5 × $21,600 = $8,640 would amortize the asset below its salvage value, so amortization expense is the remaining $1,600 that will amortize net book value to $20,000. |

|

|

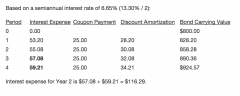

A company issues 5% semiannual coupon, 3-year, $1,000 par value bonds on January 1, 20X0, when the market interest rate is 13.3%. The sale proceeds are $800. Under the effective interest rate method, what amount of interest expense per $1,000 par value will the company record for the year ending December 31, 20X1? A)$106.40.B)$116.29.C)$66.29. |

B |

|

|

Aggressive accounting choices by management are most likely to: A)report sustainable earnings. B)comply with generally accepted accounting principles. C)produce decision-useful financial reporting. |

B Management may follow generally accepted accounting principles and still make biased (i.e., aggressive or conservative) accounting choices. Biased accounting choices diminish the decision-usefulness of financial reporting. Aggressive accounting choices are those that increase earnings, revenues, or operating cash flows in the current period (and likely reduce them in later periods). |

|

|

With regard to a firm's financial reporting quality, an analyst should most likely interpret as a warning sign a focus by management on an increase in the firm's: A)asset turnover ratios. B)pro forma earnings. C)cash from operations. |

B One potential warning sign of low-quality financial reporting is management's focus on "pro forma" or non-GAAP measures of earnings. Increases in operating cash flows or asset turnover ratios are not typically viewed as warning signs of poor financial reporting quality. |

|

|

If a firm's financial reports are of low quality, can users of the reports assess the quality of the firm's earnings? A)No, because low-quality financial reports are not useful for assessing the quality of earnings. B)Yes, because users can assess earnings quality independently of financial reporting quality. C)Yes, because if financial reports are of low quality, earnings are also of low quality. |

A Financial reports that are of low quality make it difficult or impossible for users of the statements to assess the quality of the firm's earnings, cash flows, and balance sheet values. |

|

|

Which of the following is least likely to be a motivation for managers to issue financial reports of low quality? A)Accounting controls are weak within the company. B)Enhancement of the manager's career. C)Keeping earnings above the same period in the prior year. |

A Weak accounting controls may offer an opportunity to issue low quality reports but is not in itself a motivation to do so. The other two choices are motivations that might cause management to issue low quality financial reports. |

|

|

Which of the following is most accurately described as a characteristic of a firm's quality of earnings? A)Sustainability. B)Relevance. C)Completeness. |

A Quality of earnings relates to the level and sustainability of a firm's earnings. Relevance and faithful representation (including completeness and neutrality) are characteristics of a firm's financial reporting quality. |

|

|

With regard to the goal of neutrality in financial reporting, accounting standards related to research costs and litigation losses should be viewed as: A)promoting neutral financial reporting. B)biased toward aggressive financial reporting. C)biased toward conservative financial reporting. |

C Some accounting principles, such as IFRS and U.S. GAAP standards for expensing research costs and recognizing probable litigation losses, reflect conservatism rather than neutrality, in that they require earlier recognition of probable losses and later recognition of probable gains. |

|

|

Under which inventory cost flow assumption is a firm most likely to show an unusual increase in gross profit margin by sales in excess of current period production? A)LIFO. B)FIFO. C)Average cost. |

A Under LIFO and with increasing prices, a firm that sells more goods than it purchases or produces in a period may show an unsustainable increase in gross profit margin because items recognized in cost of sales are valued older, lower prices, while sales are recorded at current, higher prices. |

|

|

FIFO ending inventory = LIFO ending inventory + LIFO reserve = 22,000 + 4,000 = $26,000FIFO after-tax profit = LIFO after-tax profit + (change in LIFO reserve)(1 − t) = $2,000 + ($1,000)(1 − 0.4) = $2,000 + $600 = $2,600 |

|

|

For 2007, Morris Company had 73 days of inventory on hand. Morris would like to decrease its days of inventory on hand to 50. Morris' cost of goods sold for 2007 was $100 million. Morris expects cost of goods sold to be $124.1 million in 2008. Assuming a 365 day year, compute the impact on Morris' operating cash flow of thechange in average inventory for 2008. |

2007 inventory turnover was 5 (365 / 73 days in inventory). Given inventory turnover and COGS, 2007 average inventory was $20 million ($100 million COGS / 5 inventory turnover). 2008 inventory turnover is expected to be 7.3 (365 / 50 days in inventory). Given expected inventory turnover, 2008 average inventory is $17 million ($124.1 million COGS / 7.3 expected inventory turnover). To achieve 50 days of inventory on hand, average inventory must decline $3 million ($20 million 2007 average inventory - $17 million 2008 expected inventory). A decrease in inventory is a source of cash. |

|

|

Income expense is reported on the income segment as a function of ? |

Market rate. Interest expense is always equal to the book value of the bond at the beginning of the period * market value at issuance . |

|

|

The inventory turnover ratio and the number of days in inventory are least likely used to evaluate the:A)age of a firm's inventory. B)effectiveness of a firm's inventory management. C)stability of a firm's inventory levels. |

Neither metric is directly relevant in evaluating the stability of a firm's inventory levels. Determining stability would presumably require other information such as purchase and sales levels, for example. The inventory turnover ratio and the number of days in inventory can be used to evaluate the relative age of a firm's inventory as well as the effectiveness of a firm's inventory management. Previous SubmitCheck for Revie |

|

|

Are changes in accounting principles and extraordinary items treated similarly in accordance with U.S. Generally Accepted Accounting Principles and International Financial Reporting Standards? Accounting principles; Extraordinary items |

Accounting principles(yes); Extraordinary items (no) Treatment of a change in an accounting principle is similar under U.S. GAAP and IFRS. Under both standards, a change in accounting principle is made retrospectively. The treatment of extraordinary items differs between U.S. GAAP and IFRS. Under U.S. GAAP, extraordinary items are reported net of tax below income from continuing operations. IFRS does not permit firms to treat transactions as extraordinary in the income statement. |

|

|

During 2007, Brownfield Incorporated purchased $140 million of inventory. For the year just ended, Brownfield reported cost of goods sold of $130 million. Inventory at year-end was $45 million. Calculate inventory turnover for the year. |

First, calculate beginning inventory given COGS, purchases, and ending inventory. Beginning inventory was $35 million [$130 million COGS + $45 million ending inventory - $140 million purchases]. Next, calculate average inventory of $40 million [($35 million beginning inventory + $45 million ending inventory) / 2]. Finally, calculate inventory turnover of 3.25 [$130 million COGS / $40 million average inventory]. |